Marcus Musson

Rugby world cup aside, there is a bit of good news starting to stir some fizziness amongst us tree huggers and, while not at shaken beer can levels, it is enough to improve the fettle and shelve the navel gazing for a while.

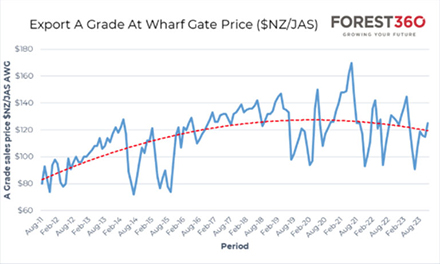

This has come in the form of an increase in export log prices which has seen November offerings in the $123-125/m3 range for A grade, up around $10/m3 on October and $30/m3 on June.

A few years ago, this price level wouldn’t have been anything to get excited about but after the lows of the past six months, it’s a welcome relief. There’s a bit of caution in this however, as the increase is not specifically demand driven and is due as much to lower shipping costs and Forex (which has since bounced) as actual sales price increases.

Real demand hasn’t really changed in terms of volume, and offtake from Chinese ports is still sitting around the 60Km3 per day. NZ supply has decreased with the lower prices and unfortunately this supply reduction is courtesy of logging contractors being slowed down, parked up or at worst going to the wall.

This current Chinese demand level isn’t likely to lift, especially with the well documented housing oversupply and litany of other economic woes that are starting to surface. It is thought that previously, construction accounted for around 70% of the softwood demand in China however, this is more likely now reduced to around 40%.

Quick Marlboro packet numbers would tell you that demand for construction-based logs has dropped 60% from pre covid times. Luckily our radiata is a very universal product and is used for a multitude of end uses.

Reduced global log supply has also helped the China supply and demand balance with logs from Europe and Russia dropping significantly in recent months.

European harvesting has receded back to normal levels as bark beetle infestation has reduced resulting in less requirement for log exports while the Russians are facing weather related issues with their seasonal harvest.

Chinese log inventory is sitting at around 2.7 million m3 which is the lowest point in years and not unexpected given the reduced overall demand.

Efforts by the CCP to inject some stimulus into the Chinese economy have seen some traditionally unconventional measures with the issuance of a $US137 billion sovereign debt plan which will take the budget deficit ratio to 3.8% of GDP, well in excess of the 3.0% target set in March this year.

While this isn’t at Grant Robertson levels yet, there is clearly a strong desire within the government to bring some confidence to the economy with stronger fiscal policy. This likely won’t do much to help the construction sector as the government has realized that can has become too big to kick down the road. Much of the stimulus has been targeted at fast growing advanced manufacturing including electric cars and semiconductors – not much wood in those.

The world has looked to China as the global economic powerhouse for decades, but it appears that India is now emerging as credible player. While India lags behind China with a $US3.5 trillion economy compared to China’s $US15 trillion, early signs are showing foreign investment pulling out of China at rapid pace and reinvesting in India.

China’s official growth target of 5% will be surpassed by India in 2023 with the IMF projecting a growth rate in the world’s most populated country of 6.3%. India is embarking on a large-scale infrastructure build with around 50,000km of new roads built in the 8 years between 2014 and 2022.

Unfortunately, NZ has been locked out of the Indian log market for a number of years as the EPA put ideology ahead of common sense with the effective banning (through unachievable recapture targets) of the use of the only India approved fumigant, Methyl Bromide in 2022.

The recent concession by India to allow fumigation at port has seen the first vessel from NZ head to India in a few years. Understandably, we are watching this with anticipation as it’s always risky to be the first to send $NZ7 million worth of cargo across the globe to test a new process however, all going well this will relieve some supply pressure from China.

After a rally in August, the NZU price has very slowly been heading in the positive direction with current spot fixtures around $70/NZU.

This is good news if you’re in the ETS as that price level represents an annual return of around $2,100/ha. Spare a thought for the ETS administrators around the country who are not so fizzy with the continued failure of MPI’s newly built online ETS administration system, Tupu-ake.

MPI kicked off this online disaster earlier this year, right at the end of a mandatory reporting period, causing massive frustration and cost for all who have the displeasure of having to use it.

This system has been plagued with problems (which makes Novapay look like a dream) and MPI officials continue to keep their heads in the sand about its efficacy. In Māori, Tupu-ake means ‘grow up’, it might be time to rename the system ‘Korenga’ meaning ‘failure’, or better still, simply bin it and go back to the old system.

In summary, we’re heading into the end of the year in better shape than many expected.

There’s talk of a number of larger forest companies taking a month out over Christmas and the windthrow salvage in Taupo, which has been running at around 15,000 tonnes per day, will start to slow leading to a lower supply and inventory position in Q1 2024.

The chances of a strong China led rebound are about as likely as David Seymour becoming a socialist, but if we can keep a lid on supply levels, we should see some price stability over the summer months. However, like the Winston factor, you never know what will come from left field…

Marcus Musson is a Forest360 director in New Zealand